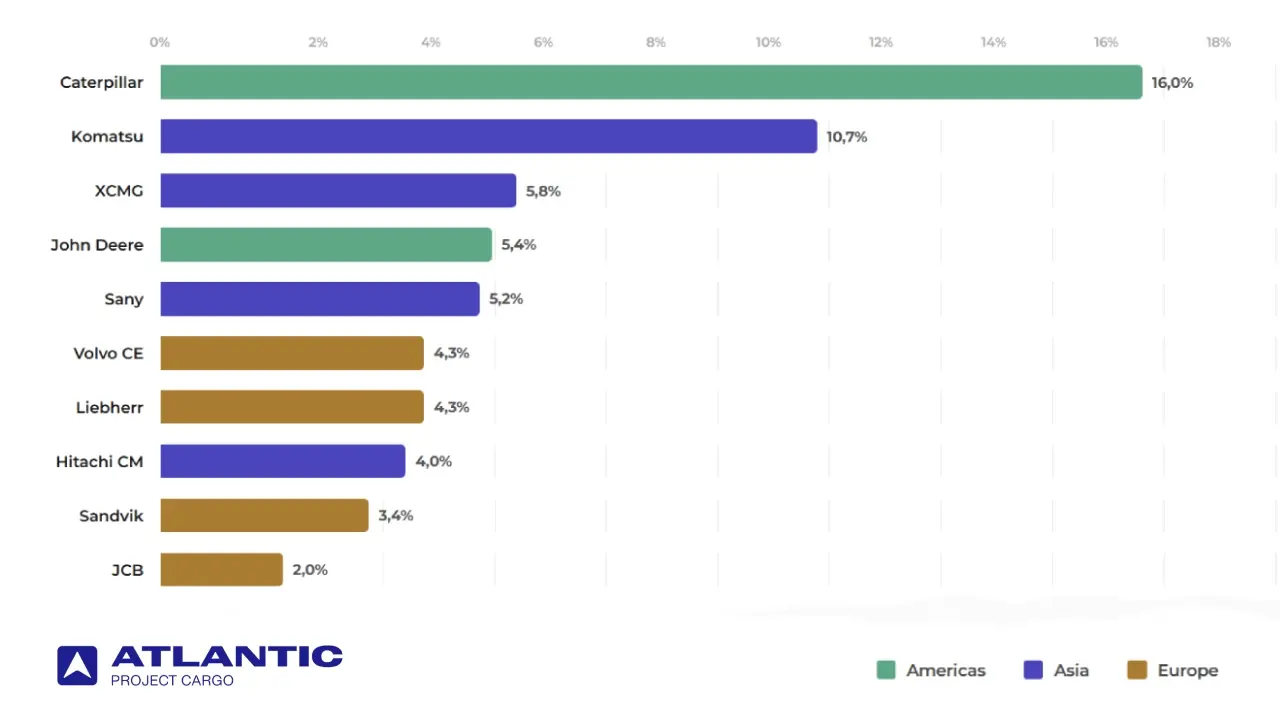

Top 10 Construction Equipment Manufacturers

June 26, 2026

Shipping Quote

Customs Duties

Drayage Rate

Nick Yadryshnikov

Nick Yadryshnikov